Why Irregular Costs Feel More Stressful Than Monthly Ones

Many households can anticipate certain expenses without knowing exactly when they will feel most inconvenient. That is where Sinking Fund Budgeting becomes useful. Instead of treating uneven costs as sudden emergencies, people set aside money gradually for categories they already know will return. The value is psychological as much as practical. Expenses feel less disruptive when they arrive as planned events rather than unwelcome surprises.

Irregular Expense Planning works because it reflects the real rhythm of life. Some costs are not monthly, yet they are not random either. Travel, home upkeep, celebrations, school needs, and seasonal household items tend to reappear. A sinking fund acknowledges that pattern and creates a place for it inside the budget before pressure builds.

Why Separate Buckets Can Make Saving Easier

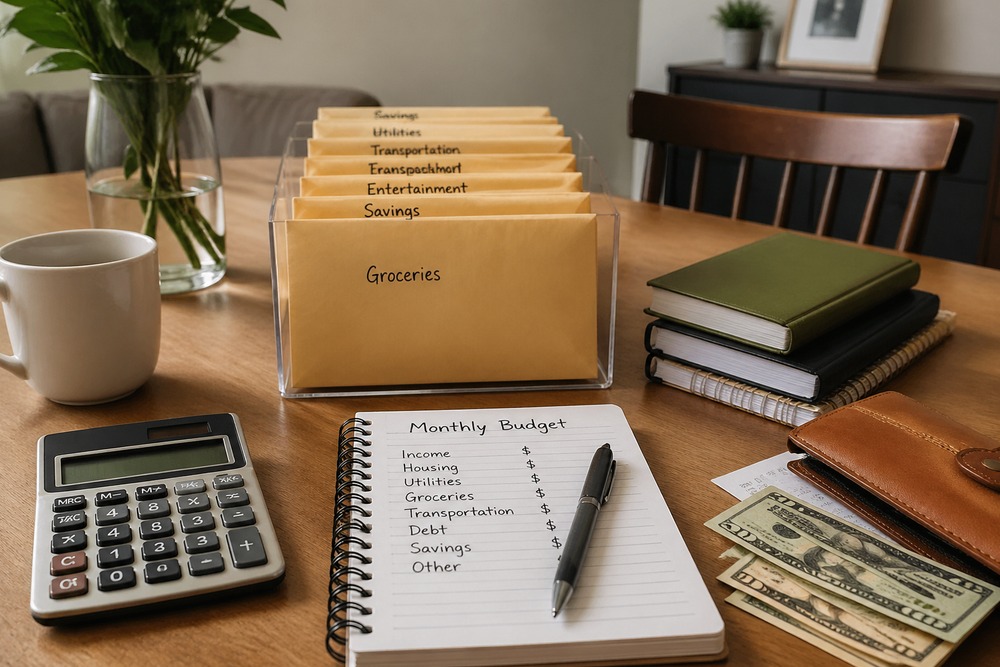

Household Saving Buckets help people give money a purpose before spending decisions compete for it. This can make budgeting feel calmer because money set aside for one future need is less likely to be mistaken for general flexibility. The system is not about creating a large number of complicated accounts. It is about separating intentions clearly enough that decisions become easier to make.

Bill Timing Awareness also improves when funds are organized by purpose. People begin to notice when certain costs tend to cluster and which periods feel tighter. That visibility can reduce the sense of confusion that comes from seeing a healthy balance one week and a strained budget the next. A clearer map of future obligations creates steadier expectations.

| Fund Type | Main Use | Planning Benefit |

|---|---|---|

| Emergency reserve | Unexpected disruption | Protects against true uncertainty |

| Sinking fund | Expected but uneven cost | Turns future pressure into a routine saving task |

| General spending pool | Daily flexibility | Keeps ordinary expenses visible |

| Seasonal category | Time-specific needs | Prepares for recurring shifts in spending |

Sinking Funds Are Not the Same as Emergency Cash

Emergency Cash Separation is important because these two kinds of money solve different problems. An emergency reserve protects against disruption that could not reasonably be planned for. A sinking fund prepares for costs that are known in advance, even if the exact timing is flexible. Confusing the two can make both systems weaker. Expected expenses consume money that should have remained available for genuine surprises.

People often feel more in control once this distinction becomes clear. A planned household repair category, for example, creates space for an expected future need without forcing every large expense to feel like a crisis. The budget becomes more honest about what life usually demands.

Timing Matters as Much as Category Choice

Seasonal Spending Prep works best when people notice patterns instead of reacting late. Some periods naturally bring more gift giving, travel, home upkeep, or school-related purchases. A sinking fund does not need perfect forecasting to help. It only needs awareness that these periods exist and are likely to return. That awareness reduces the emotional swing between calm months and crowded months.

Budget Tracking Routine keeps the system from becoming stale. Small check-ins help people see whether a category still reflects real life or whether the plan has drifted away from actual needs. A sinking fund should support flexibility, not replace it. Categories can change as circumstances change.

Progress Feels Different When Preparation Is Visible

One overlooked benefit of a sinking fund is that it makes preparation visible. Many budgeting efforts feel thankless because the work happens quietly and only reveals its value when pressure arrives. A dedicated fund changes that experience. People can see that they have already begun answering a future need, which makes the budget feel more active and less defensive. Saving becomes part of a plan rather than a vague hope that money will somehow be available later.

This visibility also helps households talk about money more calmly. When a category already exists for a future cost, the conversation shifts from alarm to adjustment. That makes decisions easier to share and easier to sustain over time.

Simple Systems Usually Last Longer

It is tempting to create a detailed structure with many categories, but a system that is too complicated can be hard to maintain. The best sinking funds are usually the ones people can understand quickly and revisit without fatigue. A few well-chosen categories often outperform a perfect-looking framework that nobody enjoys using. Sustainable budgeting depends on clarity as much as accuracy.

That is why good sinking funds are flexible. They reflect real patterns, but they are not treated as permanent architecture. When household priorities shift, the system should adapt with them.

The Goal Is a More Stable Budget Experience

Sinking Fund Budgeting is valuable because it softens the edge of uneven spending. It allows households to prepare gradually for costs they already know will matter. That kind of preparation reduces the pressure to solve everything at once when a due date appears. It also makes spending choices feel more deliberate, because money has been assigned before urgency takes over.

The broader benefit is steadiness. A budget becomes easier to trust when known future needs are given space inside it. Stability does not come from predicting every event. It comes from respecting recurring patterns and preparing for them with clarity.

Questions About Sinking Funds

What makes a cost right for a sinking fund?

An expense is a good fit when it is expected to return but does not arrive as a regular monthly bill.

Is a sinking fund only useful for large purchases?

No. It can help with any uneven cost that tends to create pressure when it arrives, even if the amount is moderate.

Why not keep all savings in one place?

Separate categories make future intentions clearer. That clarity can reduce accidental overspending and improve planning confidence.

How is this different from an emergency fund?

A sinking fund prepares for a known type of future expense, while an emergency fund protects against events that could not reasonably be planned.

Does the system need to be complex to work?

No. It works best when the structure is simple enough to maintain and specific enough to reflect real spending patterns.